Latest Posts

-

What Is a Mature Driver Improvement Course?

As experienced drivers, we understand the importance of staying up to date with the latest traffic laws, regulations, and safe driving techniques. One valuable resource available to mature drivers is a Mature Driver Improvement Course. In this blog post, we'll explore what a Mature Driver Improvement Course entails and how it can enhance safety, knowledge, and potential insurance savings for older drivers.

-

Understanding Mature Driver Auto Insurance Discounts in California: Saving on Premiums for Experienced Drivers

16 Jun, 2023As we age, our driving habits and skills evolve, often becoming more cautious and responsible. Recognizing the experience and typically lower risk associated with mature drivers, insurance companies offer special benefits known as mature driver auto insurance discounts. If you're a seasoned driver in California who is 55 or older, understanding these discounts can help you save on your car insurance premiums while enjoying the road with peace of mind.

-

Why Mature Driver Tune Up is the Best Senior Driver Safety-Improvement Course In California

With its no-test format, shorter duration, affordable pricing, and DMV-approved curriculum, **Mature Driver Tune Up** is clearly the best option for mature drivers in California. By completing this course, drivers can enjoy insurance discounts, improve their road safety skills, and save time and money in the process.

-

Car insurance rates could jump 50% in 3 states.

Car insurance rates could jump 50% in 3 states. There's some bad news ahead for the nation's car owners, with a new report forecasting that auto insurance — one of the biggest drivers of inflation this year — will continue to rise in 2024. In fact, residents of three states could see their coverage rates spike by 50% in 2024.

-

DMV Highlights New Traffic Laws In 2024

The California Department of Motor Vehicles (DMV) wants Californians to be aware of several new laws taking effect in 2024.

-

Mature Driver Courses

Mature driver courses are specialized driving courses designed for older adults to improve their driving skills, knowledge, and safety. As we age, our driving abilities change, and we may develop certain medical conditions that affect our driving.

-

Preparing to Hang Up the Car Keys as We Age

Preparing to Hang Up the Car Keys as We Age

-

How Much Can I Save by Taking a Mature Driver Course in California?

If you’re a California driver age 55 or older, you may have heard that a mature driver improvement course can help lower your auto insurance premium. A common question is: “How much can I actually save?”

-

If You're Over 65, Don't Get Behind the Wheel If You Notice This

If You're Over 65, Don't Get Behind the Wheel If You Notice This

-

How to talk to your aging parents about safe driving

How to talk to your aging parents about safe driving

-

Save Big with State Farm's Mature Driver Improvement Discount

If you're aged 55 or older, State Farm has a fantastic opportunity for you! The State Farm Mature Driver Improvement Discount is designed to reward experienced drivers like you with savings on your car insurance premiums.

-

Protect Yourself from Mail Theft In California

Protect Yourself from Mail Theft In California

-

The Best Alternative to AARP's Smart Driver Course

When you compare the options, www.MatureDriverTuneup.com stands out as the best alternative to AARP’s Smart Driver Course.

-

New California law aims to improve pedestrian safety by changing parking rules

New California law aims to improve pedestrian safety by changing parking rules. The law prohibits parking within 20 feet of any marked or unmarked crosswalk to clear the range of vision of approaching drivers

-

Why Drivers Are Choosing Mature Driver Tune Up Over AARP’s Smart Driver Course

Why Mature Drivers Are Choosing www.MatureDriverTuneup.com Over AARP’s Smart Driver Course

-

Why State Farm Customers Are Choosing the Mature Driver Tune-Up Course to Lower Auto Insurance Premiums

Why State Farm Customers Are Choosing the Mature Driver Tune-Up Course to Lower Auto Insurance Premiums

-

Why CSAA Members Are Choosing the Mature Driver Tune-Up Course to Save on Auto Insurance

Why CSAA Members Are Choosing the Mature Driver Tune-Up Course to Save on Auto Insurance

-

Top 10 Questions Drivers 55+ Ask About Mature Driver Courses

Top 10 Questions Drivers 55+ Ask About Mature Driver Courses

-

State Farm Senior Defensive Driver Discount: Why Customers Take the Mature Driver Tune-Up Course

State Farm Senior Defensive Driver Discount: Why Customers Take the Mature Driver Tune-Up Course

-

How Seniors Can Save on Auto Insurance with a Little-Known Mature Driver Discount

How Seniors Can Save on Auto Insurance with a Little-Known Mature Driver Discount

-

Mature Driver Course Insurance Discount California | Drivers 55+

Learn how a California mature driver improvement course can help drivers 55+ save up to 15% per year on auto insurance.

-

What Is a Mature Driver Improvement Course in California?

What Is a Mature Driver Improvement Course in California?

-

Complete Guide to California Mature Driver Improvement Courses (Drivers 55+)

Welcome to the complete resource for California mature driver improvement courses. This guide is designed for drivers age 55 and older who want to stay safe on the road, remain independent, and qualify for valuable auto insurance discounts.

-

How to Talk to Your Aging Parents About When to Stop Driving

How to Talk to Your Aging Parents About When to Stop Driving

-

How Mature Driver Courses Help California Drivers 55+ Save on Auto Insurance

How Mature Driver Courses Help California Drivers 55+ Save on Auto Insurance

-

Who Is Eligible for a Mature Driver Course in California?

Who Is Eligible for a Mature Driver Course in California?

-

How Often Should Seniors Take a Mature Driver Course?

How Often Should Seniors Take a Mature Driver Course?

-

Online vs In-Person Mature Driver Courses

Online vs In-Person Mature Driver Courses

-

Top Questions Seniors Ask About Mature Driver Courses

Top Questions Seniors Ask About Mature Driver Courses

-

Why Insurance Companies Support Mature Driver Courses

Why Insurance Companies Support Mature Driver Courses

-

What Seniors Learn in a Mature Driver Course

What Seniors Learn in a Mature Driver Course

-

The Hidden Auto Insurance Discount Many Seniors Miss

The Hidden Auto Insurance Discount Many Seniors Miss

-

How Mature Driver Courses Help Seniors Stay Safe

How Mature Driver Courses Help Seniors Stay Safe

-

AARP vs. Mature Driver Tune-Up: What’s the Difference for California Seniors?

AARP vs. Mature Driver Tune-Up: What’s the Difference for California Seniors?

-

Why State Farm and AAA Customers Choose Mature Driver Tune-Up

Why State Farm and AAA Customers Choose Mature Driver Tune-Up

-

Mature Driver Tune-Up vs AARP Smart Driver (AAA Members in California)

Mature Driver Tune-Up vs AARP Smart Driver (AAA Members in California)

-

Mature Driver Course vs. Defensive Driving Course: What’s the Difference in California?

Mature Driver Course vs. Defensive Driving Course: What’s the Difference in California?

-

Common Myths About Mature Driver Improvement Courses (California Drivers 55+)

Many California drivers age 55 and older have heard about mature driver improvement courses—but there’s also a lot of confusion surrounding them.

-

Benefits of Mature Driver Courses Beyond Insurance Savings (California Drivers 55+)

Many California drivers 55+ first consider a mature driver improvement course to qualify for an auto insurance discount. While the savings can be meaningful, they’re only part of the value.

-

Explore the Mature Driver Improvement Resource Library

Use the guides below to dive deeper into specific topics. Each article links back to this hub and to related resources to help you quickly find what matters most to you.

-

Why State Farm Customers Are Choosing Mature Driver Tune-Up to Get Their Senior Auto Insurance Discount

Why State Farm Customers Are Choosing Mature Driver Tune-Up to Get Their Senior Auto Insurance Discount

-

Why Farmers Insurance Customers Trust Mature Driver Tune-Up for Their Senior Auto Insurance Discount

Why Farmers Insurance Customers Trust Mature Driver Tune-Up for Their Senior Auto Insurance Discount

-

AAA Roadwise Driver Course vs Mature Driver Tune-Up: Which is Better for Senior Drivers?

AAA Roadwise Driver Course vs Mature Driver Tune-Up: Which is Better for Senior Drivers?

-

Mature Driver Course Comparison: MatureDriverTuneUp vs. AARP vs. AAA (California Guide)

Mature Driver Course Comparison: MatureDriverTuneUp vs. AARP vs. AAA (California Guide)

-

Best Mature Driver Course in California: Complete Guide

Best Mature Driver Course in California: Complete Guide

-

Mature Driver Course California

Mature Driver Course California (Complete Guide). This guide explains everything you need to know about California’s mature driver program—and how to choose the best course.

-

senior driver course california

Drivers 55+ in California can improve safety and save money with a mature driver course. Learn how it works, what to expect, and how to maximize your insurance discount.

-

Online Mature Driver Improvement Course

What Is an Online Mature Driver Improvement Course in California?

-

DMV Approved Mature Driver Course in California

DMV Approved Mature Driver Course in California

-

Senior Driving Course Online in California: A Complete Guide

Senior Driving Course Online in California: A Complete Guide

-

Cheapest mature driver course California

Find the cheapest mature driver course in California. Compare prices, features, and DMV-approved options to save money and qualify for auto insurance discounts for drivers 55+.

-

Senior Driving Class Near Me: Online vs. In-Person Options in California

Looking for a senior driving class near you in California? Learn why most courses are now online, compare online vs. in-person options, and find the easiest way to qualify for auto insurance discounts.

-

Mature Driver Insurance Discount Course: How It Works in California

Mature Driver Insurance Discount Course: How It Works in California

-

Insurance Savings Guide for Seniors: How to Lower Your Auto Insurance in California

Insurance Savings Guide for Seniors: How to Lower Your Auto Insurance in California

-

The Cost of Living Is Too High! How Much Can Seniors Save on Car Insurance in California?

The Cost of Living Is Too High! How Much Can Seniors Save on Car Insurance in California?

All Posts

Photostream

Social

Car insurance rates could jump 50% in 3 states.

Car insurance rates could jump 50% in 3 states. Here's where.

https://finance.yahoo.com/news/car-insurance-rates-could-jump-155215262.html

There's some bad news ahead for the nation's car owners, with a new report forecasting that auto insurance — one of the biggest drivers of inflation this year — will continue to rise in 2024. In fact, residents of three states could see their coverage rates spike by 50% in 2024.

That's according to a new report from Insurify, a company that provides data about auto insurance rates. The typical U.S. insurance policy will jump 22% this year to an average annual premium of $2,469 by year-end, the report found. That comes after drivers saw their policies jump 24% in 2023, it noted.

The three states where insurance rates could jump by more than 50% this year are California, Minnesota and Missouri, the Insurify report found. Drivers in those states could see their rates rise by 54%, 61% and 55%, respectively.

Auto insurance remains a pain point for consumers after experiencing more than two years of elevated inflation. And even as the overall inflation rate is cooling — the Consumer Price Index dropped to 2.9% in July, the first time since March 2021 it's dropped below 3% — drivers are continuing to see their policy rates rev up, fueled by more climate events that are causing vehicle damage.

"Increasingly severe and frequent weather events are driving up auto insurance premiums," Insurify said in its report. "Hail-related auto claims represented 11.8% of all comprehensive claims in 2023, up from 9% in 2020, according to CCC Intelligent Solutions."

Drivers in Maryland currently pay the highest average rate, at $3,400, for annual full coverage as of June, the Insurify analysis found. Their rates are projected to jump 41% to $3,748 by year-end, it noted. The second most expensive state is South Carolina, with an average policy premium of $3,336 in June. That could rise by 38% to $3,687 by the end of the year.

As CBS News has reported, there are a few additional reasons, aside from climate events, that are driving up auto rates — even if your driving record hasn't changed.

First, the costs paid by insurance providers to repair vehicles after an accident, such as for labor and parts, have increased more than 40%, and insurers are passing those increases onto drivers. Secondly, because lawyers are more often involved in handling accident claims than in prior years, settlements are increasing, which also boosts insurance costs.

Some drivers are avoiding filing claims

The surge in auto insurance rates is prompting drivers to change their behavior, according to a new report from LendingTree.

About 4 in 10 insured drivers who have been in an auto accident or incident have skipped filing a claim with their insurance company, its survey of 2,000 U.S. consumers found. About one-quarter of drivers who filed a claim said they later regretted it.

Drivers who avoided filing a claim said they did so because the damage was minimal or the deductible was higher than the cost to fix their vehicle. But another 42% said they skipped an insurance claim because they didn't want their rates to jump.

"Once you've been involved in an accident of any type, insurance companies see you as riskier to insure," LendingTree auto insurance expert and licensed insurance agent Rob Bhatt said in a statement. "Your rates will eventually come down if you avoid claims for three to five years, depending on your insurance company. But you're going to feel a financial squeeze until then."

Still, Bhatt said it's typically worth filing a claim if the repairs will cost a few thousand more than your deductible, even if your rates subsequently rise.

"The whole point of having car insurance is to prevent an accident from leaving you in financial hardship," he said.

About

Mature Driver Tune-Up® is a California company headquartered in Redwood City, California, dedicated to helping drivers age 55 and older stay safe on the road while qualifying for valuable auto insurance savings.

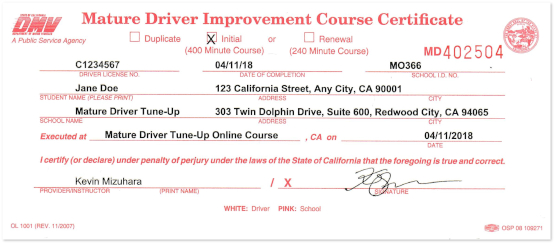

Our California DMV-approved Mature Driver Improvement Courses are designed specifically for California drivers—not as one-size-fits-all national programs. After successfully completing the course, you'll receive your Official California DMV Mature Driver Improvement Certificate, which is accepted by all California auto insurance companies for eligible mature driver discounts.

Our mission is simple: provide an easy, convenient online course that helps experienced drivers refresh their driving knowledge, build confidence behind the wheel, and continue enjoying the benefits of safer driving and potential insurance savings.

California DMV Mature Driver Improvement License #: MDIP000069

Recent Blog Entries

Contact Us

Online Course Only (No In-Person Courses)

Phone and Email Support Hours:

• Mon-Thu 8:00-5:00 PT

• Fri 8:00-4:00 PT

Phone: (800) 414-5587

Email: support@mdtuneup.com

Stay Connected

Privacy Policy | Terms of Service | Mature Driver Tune-Up, CA DMV License #MDIP000069